The theory of corporate financialization centers around the idea that shareholders have become the dominant stakeholders in the decision-making process of public companies and wider society, that their returns have become the sole goal of firm strategy and that their interests are placed above those society as a whole.

One central outcome is that the share of firm income distributed to shareholders has been increasing over the last decades. Corporate financialzation is best measured by the toll that shareholders extract from firms simply for being their owners, or as Keynes called them, functionless investors or rentiers.

Let’s start from an observation

Civil society, the media and scholars are increasingly aware of this increase in shareholder prominence, but it is misunderstood how precisely they come to claim an increasing share of firm income. The how might sound trivial, but I will show that the answer to this basic question is (a) counterintuitive and surprising, (b) a fundamental first step in the process of establishing the causality of some of the central hypothesized effects put forward by the corporate financialization literature and (c) an overlooked requirement for understanding the why — and why not.

People tend to focus on large increases in dividends or share repurchases (payouts), but I show that it is not the growth of shareholder remunerations that causes rising payout ratios, but precisely their inability to fall, their downward rigidity.

This is an extremely short summary, the full article - as well as the appendix with additional figures - can be found here.

No Bonanza, but downward rigidity

While firms may slightly increase payouts when profits are high, they are reluctant to reduce them when profits fall. Payouts thus seem to - just like a ratchet - fractionally adjust upwards in good times but to be downward rigid in bad times, they are downward sticky.

During crises, the firm becomes a battleground for competing interests among shareholders, workers, management, and other stakeholders. It is in these moments of scarcity - when profits decline, that shareholder power kicks in: they often manage to maintain their payouts in absolute levels, thereby increasing them as a share of the firm’s income. This results in a higher payout ratio, not just momentarily, but persistently over the ensuing years. Consecutive ratchet events fuel the rise of payout ratios over time and ratchet behaviour underscores the dominant position of shareholders in the corporate hierarchy, reflecting the principles of Shareholder Value Orientation

Why this persistence?

Profits recover slowly after a negative shock, which means that keeping payouts steady implies a higher payout ratio for as long as profits have not fully recovered.

Payouts tend to fractionally adjust upwards as profits increase. This means that during the recovery, a fraction of that recovery is allocated to shareholders, such that even with a swift recovery, the payout ratio will stay higher for longer.

Ratchet events have consequences that are dynamic. If the gap in cash created by ratchet events is covered by increasing debts, the sale of assets or the reduction of investments, the ratchet event reduces future potential profits, decelerates trend growth rates, and — ceteribus paribus — keeps the payout ratio at persistently higher levels.

Firm profits are subject to heavy fluctuations and a ratchet event is no singularity. If a firm — for whatever reason — feels compelled to ratchet during profit troughs, ratchet events can and do occur multiple times. Given the slow reversal of the payout ratio after each ratchet decision, each consecutive ratchet event pushes the ratio to new highs.

Three ways to show that downward rigidity leads the upward mobility

Using data on all stock-listed firms in the world, this paper aims to connect the macro-level process of financialization with its micro-level foundations by demonstrating how SVO as a governance practice effectively translates into rising payout ratios. It shows that it is not rising payouts that should attract our attention, but rather their inability to fall. In the paper I develop the argument in three different ways: theoretically, visually and econometrically. Here I summarise the main findings.

- A model that illustrates it can

- Data visualization that suggests it might

- A staggered DiD methodology that shows it does

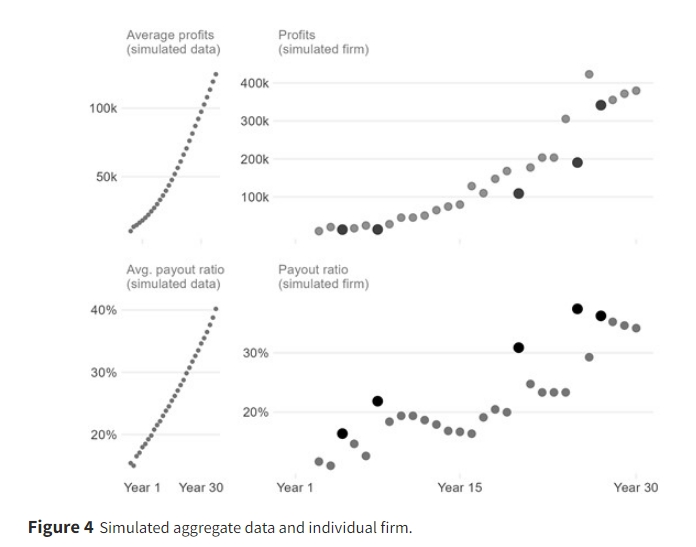

1) A model that illustrates it can

A stochastic model of ratchet behavior illustrates how fluctuations in profits, combined with the downward rigidity of payouts, fuel the upward trajectory of aggregate payout ratios over time.

At the firm level, each negative shock accompanied by the unwillingness of shareholders to yield ground ratchets up the payout ratio persistently. Despite the fact that payout ratios almost solely rise when profits fall, and fall when profits rise, on aggregate, a smooth upward trend in both profits and payout ratios emerges. Even though shocks to the system are symmetric around zero — and thus on aggregate disappear leaving only the smooth upward trend — and that payout ratios fall whenever profits rise, the resulting payout ratio inherits a strong upward trend from the occasional negative shocks. It is the fluctations in profits and the downward rigidity of payouts that induce the upward trend in the aggregate payout ratio.

This model illustrates the counterintuitive proposition central to this article: that payout ratios rise almost exclusively due to downward rigidity — when profits fall— and that despite profits generally increasing, payout ratios increase as well due to periodic shocks and slow - new - mean reversal.

2) Data visualization that suggests it might

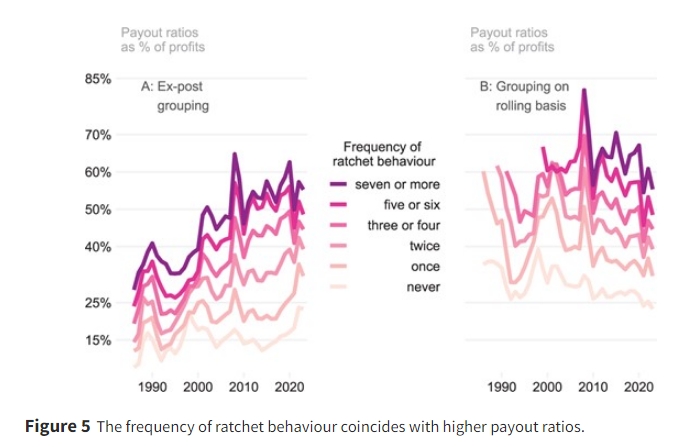

Panel A in Figure 5 groups the — real — firms according to the frequency they display ratchet behaviour and shows each group’s aggregate payout ratio over time. The payout ratio is clearly structured based on the frequency a company displays ratchet behaviour. The more often it does so, the higher the payout ratio tends to be. Panel A is a static representation of the ratchet effect, it calculates the ex post frequency of ratchet behaviour, constructs groups on the basis of the ex post number of ratchet occurrences, and then calculates the evolution of payout ratios within each group. In panel B, each firm starts in the “never” category and only switches to the next category on the year it exhibits ratchet behaviour. Then it stays in that category until the moment it undergoes an additional ratchet event, at which point it switches to the next category. For example, a company that in panel A is categorized as “seven or more”, will first have to pass through all other categories in panel B.

One can clearly see that each ratchet occurrence shifts the payout ratio upwards. While the stratification in panel A might be coincidence, panel B shows that in all likeliness, it is indeed ratchet behaviour that drives the upward shift in the payout ratio.

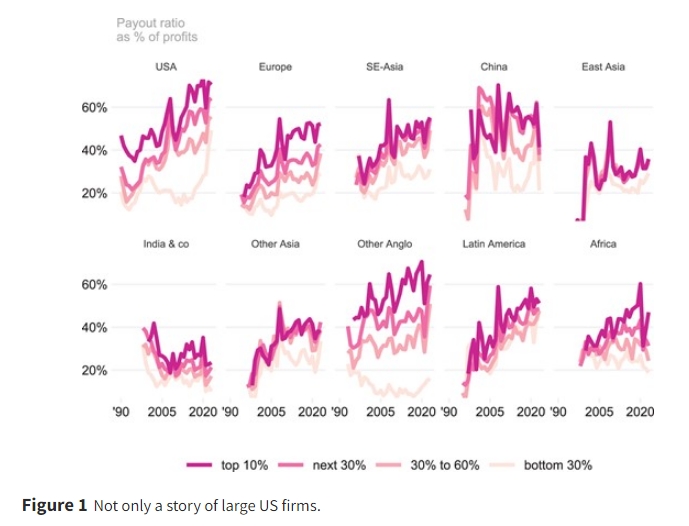

This stratification pattern with respect to ratchet behaviour keeps clearly emerging when splitting the population in groups based on size, age, sector or geographical region of the firms (see the Supplementary Appendix), which is a first indication that ratchet behaviour is a more fundamental feature of rising payout ratios than these firm characteristics

Still, while compelling, an aggregate view might not reflect the behaviour of individual firms. For the hypothesis to be true, this aggregate observation needs to stem from individual firm behaviour. At the firm level, each ratchet event should not only cause a temporary surge in the payout ratio, but also cause it to stay more elevated in the ensuing years. This firm level persistence is the key to showing that SVO indeed manifests as ratchet behaviour.

3) A staggered DiD methodology that shows it does

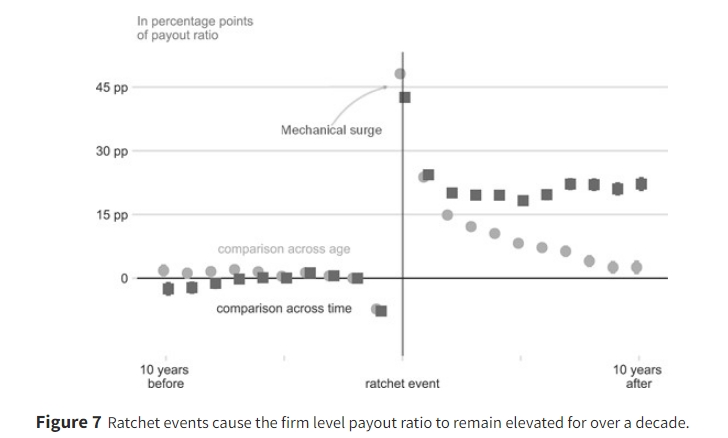

When a firm displays ratchet behaviour it makes the discrete decision to keep payouts steady in the face of falling profits. The implication that other decisions can be made and are indeed made allows for a quasi-experimental econometric design, in which some firms are treated with a ratchet decision and others are not. This econometric design allows us to exploit the differences in the outcomes of treated versus untreated firms - i.e. the ratcheting firms versus those that do not - in order to infer what the impact of the ratchet event is on the payout ratio.

More information on the methodology - as well as more results - can of course be found in the paper, but this staggered difference-in-differences methodology confirms that firms exhibiting ratchet behavior display significantly higher payout ratios compared to their non-ratcheting counterparts. Crucially, the results shown in the Figure hereunder show that the payout ratio among firms that do exhibit ratchet behaviour does not simply jump higher on the year of the ratchet event, but that it remains higher than their non-ratcheting peers for close to a decade. Finally, note the strength of the effect, which can be interpreted as the average percentage point deviation among ratcheting firms with respect to non ratcheting firms, while taking firm and time fixed effects.

Implications and further work

I find that it is not rising payouts that lead to rising payout ratios, but precisely their inability to fall. This downward rigidity constrains firms’ decision-making, particularly during economic shocks, and drives up payout ratios persistently.

This likely has real consequences. When firms maintain stable payouts despite declining profits, they must either resort to cutting investments, R&D expenditures, or labor costs or to taking on higher levels of (unproductive) debt. This can potentially stifle innovation and growth at the firm level, but also aggregate demand and productivity growth at the level of the economy.

The identification of ratchet behavior as the prime behavioural expression of shareholder primacy provides a new lens through which to examine the causes and consequences of financialization more rigourously. These will be more closely examined in follow-up research.

One thing is however clear, it is when resources become scarce that shareholder power - or primacy - really kicks in. When it does, firm income is lastingly redistributed in favour of shareholders and - likely - at the expense of other stakeholders and the wider economy.